Inside Authorization Webs: How Merchant Setup Foundations Power Stable Recurring Charge Flows Across Mobile Retail Channels

Merchant account configurations form the structural base that supports authorization sequences across payment networks, and these foundations determine whether recurring charges maintain stability when processed through mobile retail systems. Data from payment processors indicates that properly structured merchant profiles reduce authorization declines by aligning account parameters with expected transaction patterns in subscription models.

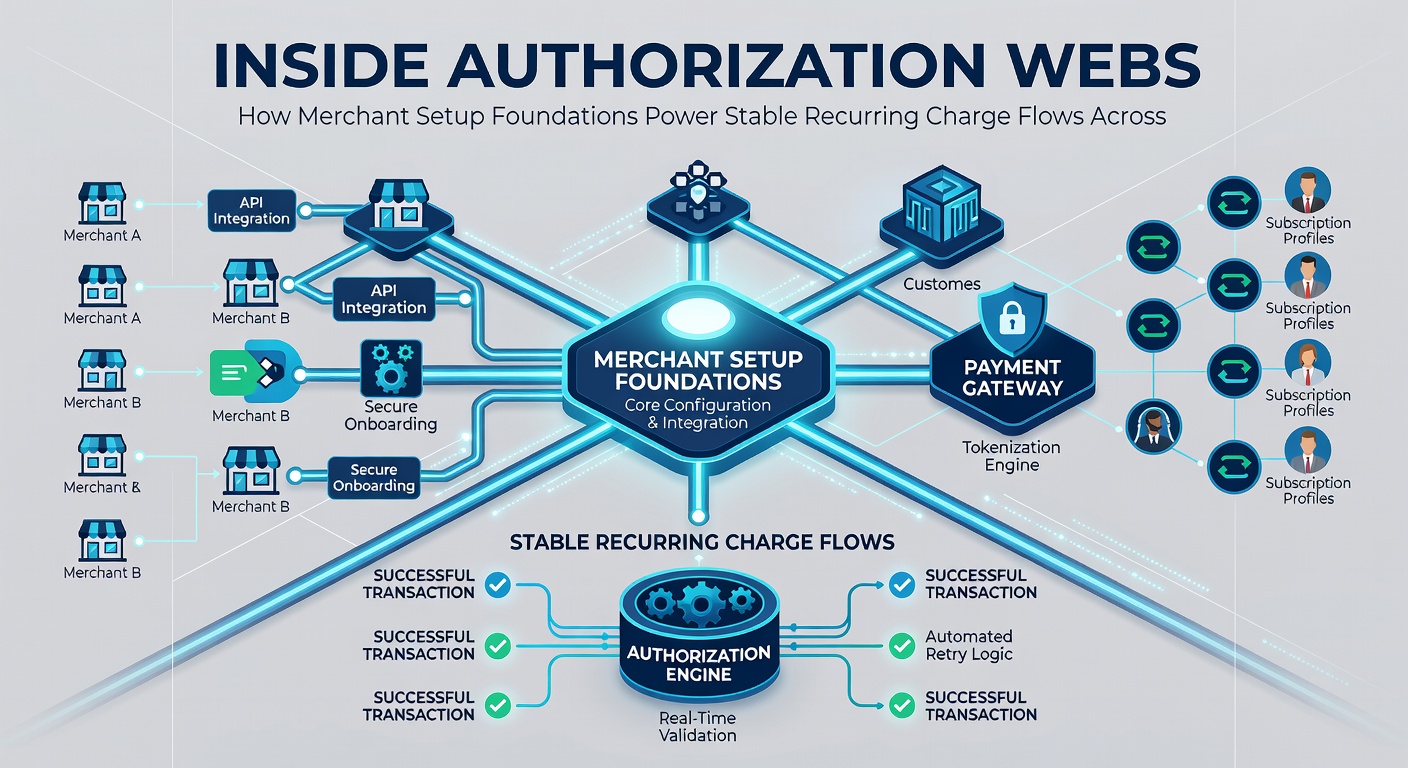

Core Elements of Merchant Account Establishment

Account creation begins with verification of business credentials and integration of processing terminals, while underwriters evaluate risk profiles based on historical sales volume and industry classification. These steps establish the parameters that later govern token issuance and recurring billing cycles, and they connect directly to the gateways that handle mobile point-of-sale interactions.

Once approved, the merchant receives identifiers that route transaction requests through acquirer banks and card networks, and these identifiers carry flags that signal recurring versus one-time charges. Observers note that mismatches in these flags often trigger holds, whereas accurate setup allows seamless continuation of scheduled payments.

Authorization Pathways in Recurring Mobile Transactions

Authorization occurs when a mobile application initiates a charge request that travels from the device through the merchant gateway to the issuing bank, and the response returns an approval code that confirms available funds or credit. In recurring scenarios the system reuses stored credentials rather than capturing new card details each cycle, which reduces friction and maintains continuity across billing periods.

Researchers have tracked how initial authorizations establish velocity limits and address verification settings that apply to subsequent charges, and these controls help sustain flow without repeated customer intervention. When merchant profiles include clear recurring descriptors, networks apply consistent rules that support higher approval rates in mobile environments.

Integration Between Merchant Foundations and Mobile Retail Channels

Mobile retail systems rely on APIs that link point-of-sale hardware to backend billing engines, and merchant setup determines which endpoints receive the necessary permissions for recurring operations. Proper configuration allows a single account to process both in-store swipes and scheduled mobile renewals without separate onboarding steps.

Studies conducted by academic institutions such as the Federal Reserve show that unified merchant identifiers correlate with lower processing interruptions across blended channels. The same identifiers carry the compliance markers required for token storage, which enables future charges to bypass full card data transmission on each mobile transaction.

Factors That Sustain Charge Stability

Stability depends on alignment between merchant category codes, recurring billing indicators, and network-level fraud filters, and these alignments prevent unnecessary declines during renewal cycles. When setups include updated contact details and accurate tax identifiers, issuers maintain clearer records that support continued authorization over extended periods.

Industry reports from the European Central Bank highlight that merchants who maintain current account documentation experience fewer disruptions in automated billing sequences. Mobile retail environments amplify this effect because transaction volumes fluctuate daily, requiring consistent backend parameters to accommodate variable demand.

Operational Practices Across Payment Networks

Networks apply rules that reference the merchant's original setup data each time a recurring request arrives, and these references determine whether the charge proceeds or requires additional verification. Accurate initial registration reduces the frequency of secondary challenges, which keeps charge flows uninterrupted across multiple billing intervals.

Payment processors document cases where merchants updated their profiles mid-cycle and subsequently saw improved authorization consistency on mobile devices. These updates typically involve refining descriptor fields and adjusting risk thresholds to match observed transaction patterns in recurring models.

Conclusion

Merchant setup foundations establish the routing rules and compliance markers that enable stable recurring charges through mobile retail channels, and they continue to influence authorization outcomes long after initial account creation. Data indicates that attention to these foundational elements supports consistent processing across card networks and mobile gateways.