Navigating API Routes for Fraud-Resistant Recurring Payments in Mobile POS Merchant Systems

Modern payment ecosystems rely on precise API pathways that connect merchant accounts directly to recurring mobile processing capabilities within point-of-sale networks, and these connections incorporate multiple layers of fraud resistance at each junction. Researchers have mapped these routes through detailed examinations of tokenization protocols and real-time verification layers that operate across mobile terminals and backend merchant systems. Data from industry analyses shows steady growth in such integrations as businesses expand recurring billing models into physical retail environments.

Core Components of API Pathways in POS Networks

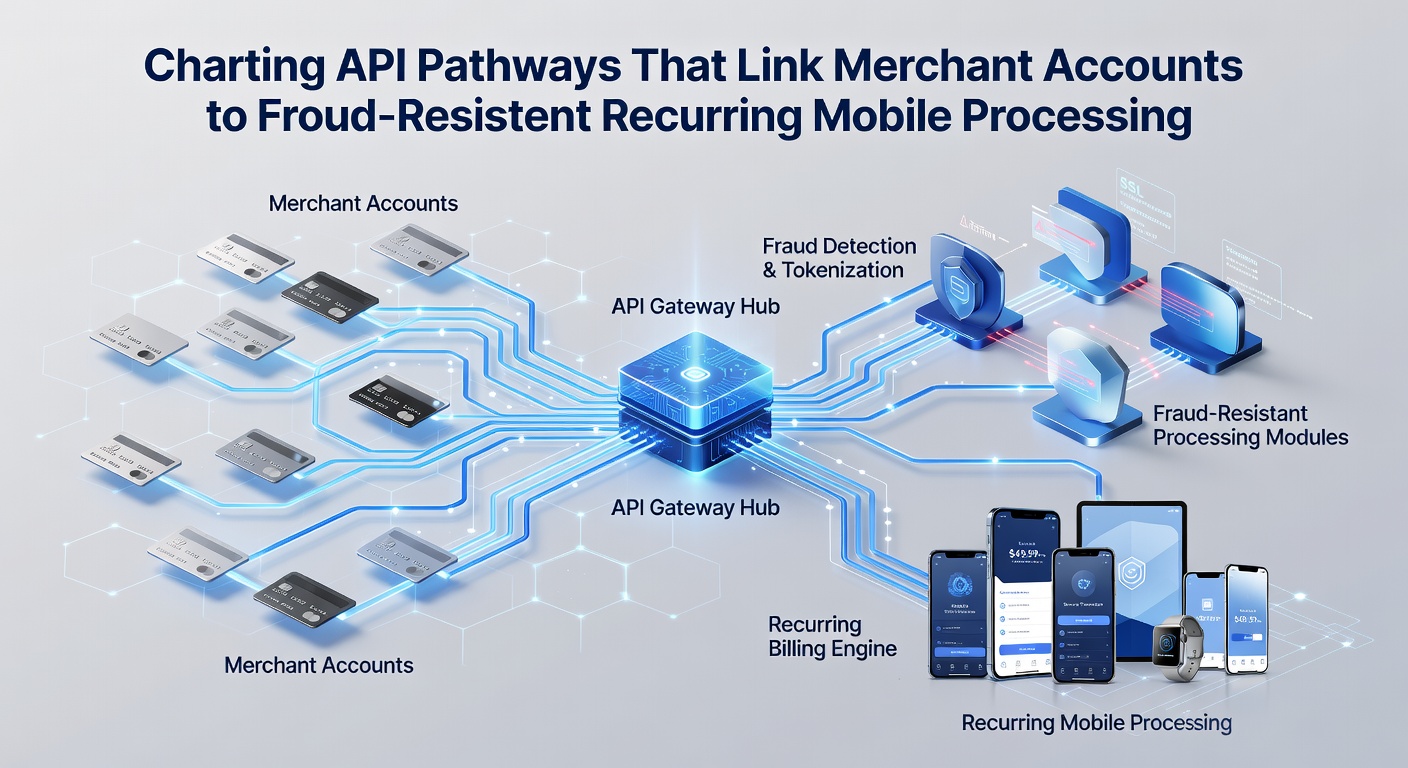

APIs serve as the structural links that allow merchant accounts to authorize recurring charges initiated from mobile devices integrated with POS hardware, and the process begins when a customer registers payment details at the terminal. Secure token exchange replaces sensitive card data with unique identifiers that travel through encrypted channels back to the merchant processor, which maintains compliance standards established by payment card networks. Studies conducted by academic institutions in North America highlight how these pathways reduce exposure points by limiting direct access to primary account numbers during repeated transactions.

POS networks incorporate geolocation checks and device fingerprinting as standard API calls that occur before each recurring authorization, and these steps help distinguish legitimate mobile activity from suspicious patterns. Figures released in regulatory updates from the European Central Bank indicate that systems employing such layered verifications experience measurable declines in unauthorized recurring attempts across participating merchant platforms. The pathways extend further when mobile apps sync with cloud-based merchant dashboards, enabling automatic updates to billing schedules without manual intervention at the store level.

Fraud Resistance Mechanisms Embedded in Recurring Mobile Flows

Fraud-resistant features within these API structures include dynamic risk scoring that evaluates transaction velocity, device history, and behavioral signals before approving each recurring charge, and this scoring runs continuously in the background of mobile POS interactions. Observers note that integration of machine learning models at the API level allows for adaptive thresholds that tighten during peak periods or in regions with elevated threat indicators. According to reports from the Australian Payments Network, merchants adopting these models report consistent improvements in detection rates for anomalies tied to mobile-initiated subscriptions.

Token lifecycle management forms another critical segment of the pathway, where APIs trigger automatic rotation of tokens after defined intervals or upon detection of potential compromise, and this rotation occurs without disrupting active recurring agreements on the merchant side. Research papers from Canadian universities detail case examples where such automated processes prevented escalation of fraud incidents that originated from compromised mobile endpoints. The pathways also route data through centralized monitoring hubs that aggregate signals from multiple POS locations, creating a unified view that flags coordinated attacks across merchant accounts.

Developments Observed Through Mid-2026

By May 2026, payment networks had expanded support for standardized API endpoints that specifically address recurring mobile processing, allowing merchant accounts to activate these features through streamlined onboarding sequences at the POS level. Regulatory guidance from bodies such as the Reserve Bank of India emphasized the importance of open API frameworks that maintain fraud controls while supporting cross-border recurring transactions. Those who have implemented these updated pathways report smoother synchronization between in-store device logs and online billing records, which reduces reconciliation errors during monthly settlement cycles.

Trade associations in the Asia-Pacific region have documented increased collaboration between software providers and hardware manufacturers to embed fraud-resistant modules directly into mobile POS firmware, and this embedding occurs through API calls that authenticate each module before activation. The result is a more resilient network where recurring charges initiated on mobile devices carry verified merchant account credentials from the initial setup onward. Evidence from these implementations shows particular strength in environments handling high volumes of subscription-based services alongside traditional retail sales.

Conclusion

API pathways that connect merchant accounts to fraud-resistant recurring mobile processing continue to evolve within POS networks through incremental refinements in verification protocols and data routing. These structures support scalable operations for businesses managing both one-time and recurring revenue streams, with security measures distributed evenly across each connection point. Ongoing documentation from global payment organizations provides reference points for merchants seeking to align their systems with current standards in mobile transaction handling.