Tracing Authorization Routes in Credit Card Networks and Mobile Subscription Billing Systems

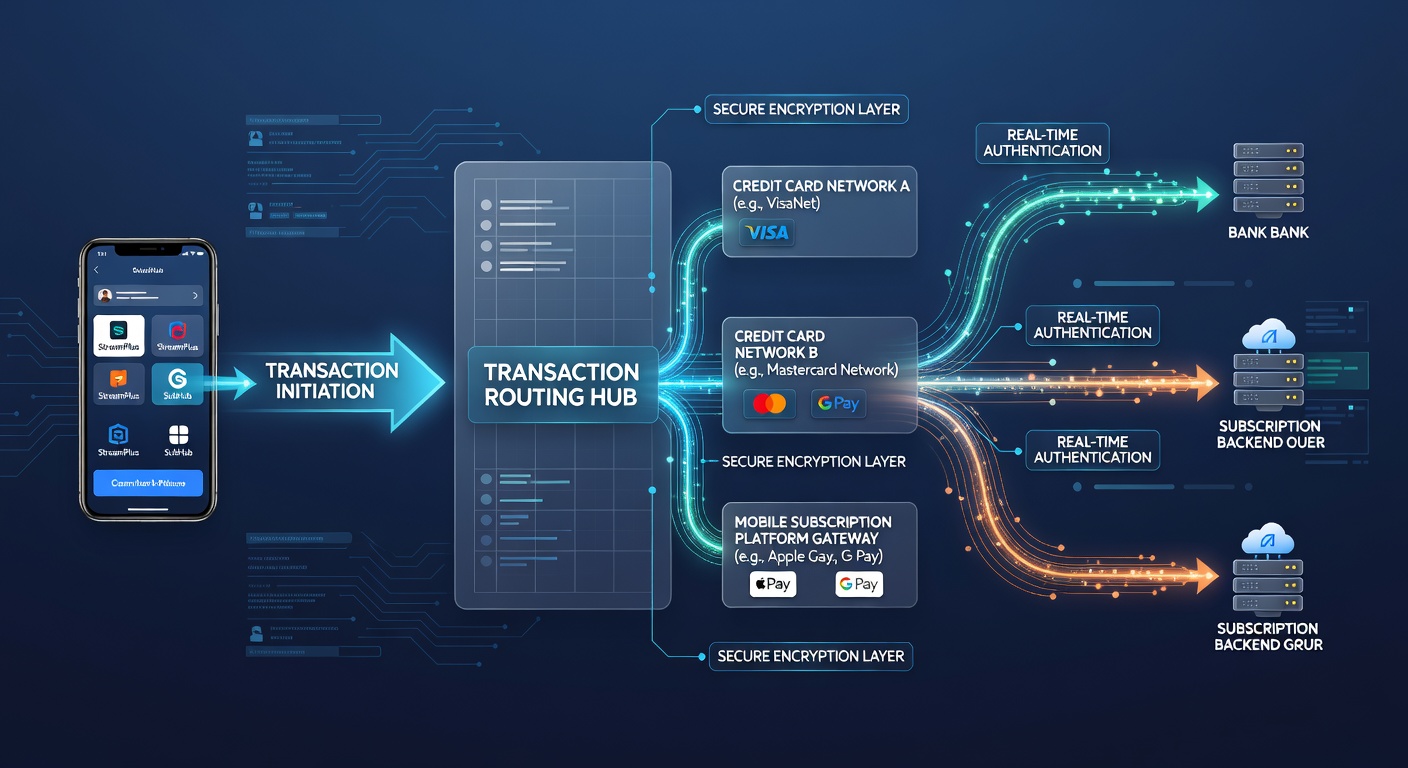

Transaction routing mechanisms determine how payment requests travel from merchants or app providers through intermediaries to card issuers or billing systems, and data from industry reports shows these pathways rely on standardized protocols that balance speed, cost, and security across global infrastructures. Credit card networks such as Visa and Mastercard operate centralized switches that evaluate each authorization request based on factors including BIN ranges, merchant category codes, and real-time risk scores before directing the message onward. Acquirers initiate the process by packaging transaction details into ISO 8583 formatted messages that networks then parse to select optimal routes, and this selection often incorporates dynamic rules that account for interchange fees along with regional regulations. Issuers receive the routed request, perform balance checks or fraud screenings, and return responses through the same network path, which keeps average authorization times under two seconds in most high-volume corridors according to Federal Reserve payment studies. Mobile subscription platforms add another layer where billing requests originate from app stores or carrier systems rather than physical terminals, and these platforms route recurring charges through dedicated APIs that connect directly to payment processors or card networks. Apple and Google maintain their own billing pipelines that enforce specific routing logic for subscription renewals, while direct carrier billing in regions like parts of Asia routes charges through mobile network operators before they reach card schemes.

Transaction routing mechanisms determine how payment requests travel from merchants or app providers through intermediaries to card issuers or billing systems, and data from industry reports shows these pathways rely on standardized protocols that balance speed, cost, and security across global infrastructures. Credit card networks such as Visa and Mastercard operate centralized switches that evaluate each authorization request based on factors including BIN ranges, merchant category codes, and real-time risk scores before directing the message onward. Acquirers initiate the process by packaging transaction details into ISO 8583 formatted messages that networks then parse to select optimal routes, and this selection often incorporates dynamic rules that account for interchange fees along with regional regulations. Issuers receive the routed request, perform balance checks or fraud screenings, and return responses through the same network path, which keeps average authorization times under two seconds in most high-volume corridors according to Federal Reserve payment studies. Mobile subscription platforms add another layer where billing requests originate from app stores or carrier systems rather than physical terminals, and these platforms route recurring charges through dedicated APIs that connect directly to payment processors or card networks. Apple and Google maintain their own billing pipelines that enforce specific routing logic for subscription renewals, while direct carrier billing in regions like parts of Asia routes charges through mobile network operators before they reach card schemes.Core Components of Credit Card Routing

Network switches apply a series of decision trees that prioritize factors such as least-cost routing when multiple network paths exist, and observers note that European markets frequently employ additional rules tied to SEPA instant payment frameworks managed by the European Central Bank. Transaction data packets carry fields that indicate whether a payment qualifies for specific interchange categories, which influences the final route selection and settlement timing.

Tokenization services further complicate routing because tokenized credentials must be detokenized at designated points within the network before the issuer can process the request, yet this step occurs seamlessly within milliseconds through pre-established secure channels. Research from the Bank for International Settlements indicates that cross-border routes add extra verification hops that can extend processing windows by 300 to 800 milliseconds depending on the corridor.

Routing Within Mobile Subscription Ecosystems

Subscription platforms maintain separate routing tables that distinguish between one-time purchases and recurring billing events, and these tables often incorporate fallback logic that redirects failed attempts to alternative processors when primary paths encounter capacity limits. App stores enforce strict validation sequences that route initial subscription setups through their proprietary gateways before any recurring authorization reaches the card networks.

Carrier billing systems in markets such as Australia rely on partnerships with the Australian Payments Network to route charges through established financial messaging standards, and this integration allows seamless handoffs between telecom infrastructure and banking rails. Renewal attempts that occur at scale require batching mechanisms that aggregate multiple subscriber requests into single network transmissions, which reduces per-transaction overhead while maintaining individual authorization integrity.

Integration Points and Data Exchange Standards

Points of convergence between credit card networks and mobile platforms occur primarily at processor level where unified APIs translate subscription metadata into card authorization formats, and these translations preserve essential fields such as recurring payment indicators that issuers use to apply tailored risk models. Standards like EMVCo specifications govern how contactless mobile payments traverse networks, ensuring consistent routing behavior whether the transaction originates from a phone wallet or a traditional card. Developments scheduled for May 2026 include updates to network routing tables that incorporate new data elements for subscription lifecycle management, allowing issuers to distinguish trial periods from active renewals with greater granularity. These changes build on existing frameworks and require acquirers along with mobile billing providers to update message specifications accordingly. Technical observers highlight that latency-sensitive routing decisions now incorporate machine learning models trained on historical approval patterns, which enables predictive path selection that minimizes declines in subscription scenarios. Geographic variations persist because regulatory environments in different jurisdictions impose distinct data residency requirements that affect where routing decisions can be executed.

Conclusion

Transaction routing across credit card networks and mobile subscription platforms continues to evolve through incremental protocol enhancements that maintain compatibility while accommodating new billing models, and the mechanisms described reflect established industry practices that support reliable authorization flows worldwide. Continued coordination among networks, processors, and platform operators ensures these systems adapt to changing transaction volumes without compromising processing integrity.