Tracing Transaction Trails: How Coordinated Systems Handle Credit Card Authorizations and Prevent Fraud Across Retail POS Networks With Automated Renewals

Retail environments rely on intricate networks that trace every step of a credit card transaction from the initial swipe or tap through final settlement, and these pathways become especially complex when automated renewals enter the picture. Systems coordinate authorizations by routing data between merchant terminals, acquirers, card networks, and issuers in milliseconds, while fraud detection layers scan for anomalies at each hop. Observers note that the process maintains accuracy across high volumes because protocols standardize message formats and response codes, allowing quick identification of issues like insufficient funds or mismatched addresses.

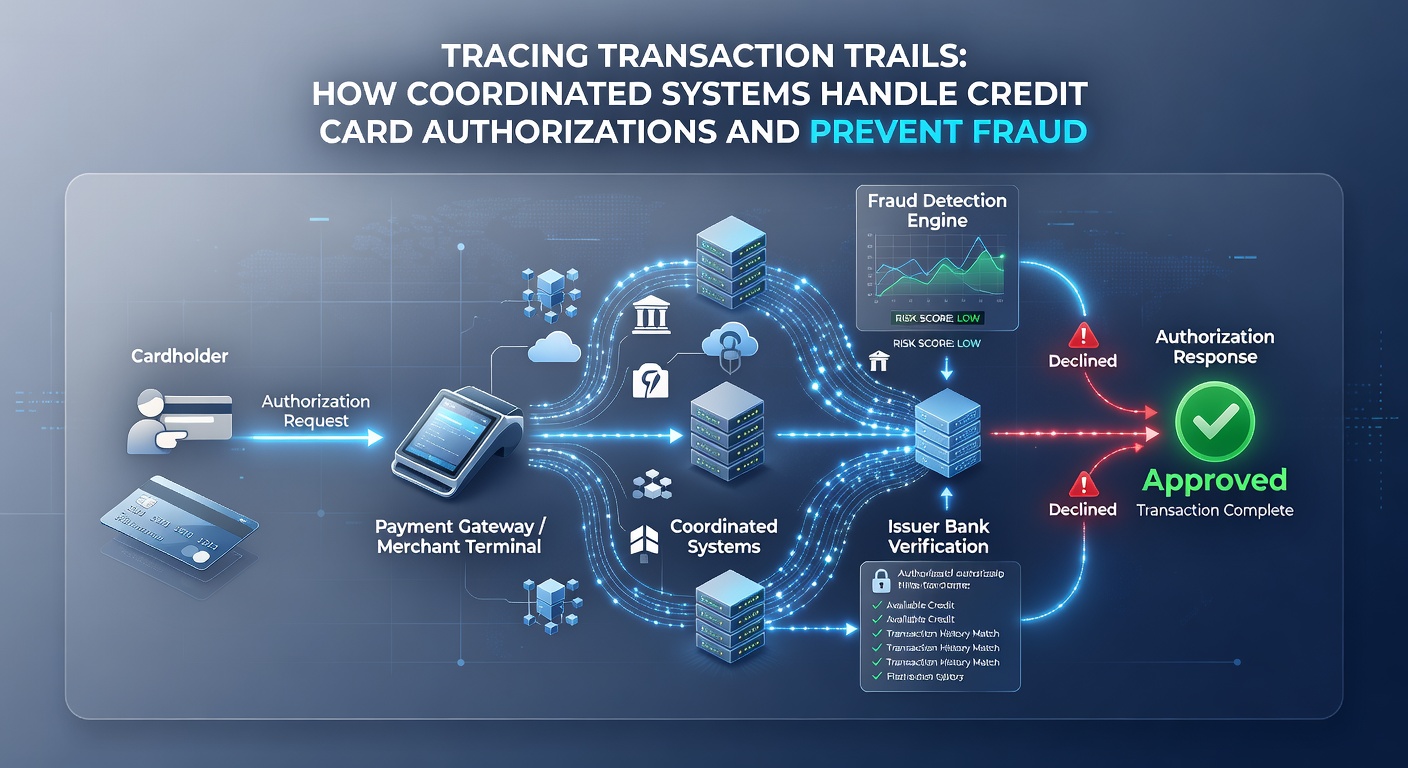

Core Mechanics of Authorization in Point-of-Sale Networks

Point-of-sale terminals initiate authorizations by encrypting card data and sending requests through secure channels to payment processors, which then forward details to the issuing bank for approval decisions. The trail records timestamps, terminal identifiers, and merchant category codes along with response values, creating an auditable path that investigators can follow if disputes arise later. Coordinated systems handle these flows by maintaining synchronized databases that update in near real time, ensuring that each participant sees consistent status information. Data shows that such synchronization reduces duplicate charges adn supports seamless handoffs when transactions move between in-store and recurring billing components.

Automated renewals add another dimension because they trigger without customer presence at the terminal, requiring stored credential protocols to reference the original authorization trail for continuity. Processors validate that recurring requests match prior transaction patterns before releasing funds, and networks apply velocity checks to flag sudden spikes in activity. Researchers have documented how these checks integrate with address verification and card verification value matches to strengthen the overall chain of custody for each payment record.

Building Fraud Detection Through Coordinated Data Trails

Fraud prevention emerges from layered analytics that examine authorization trails for deviations in spending geography, device fingerprints, and timing sequences across retail networks. When a coordinated platform receives a request, it cross-references historical data points from the same cardholder profile while applying machine learning models trained on millions of prior transactions. Studies indicate that this approach catches unauthorized attempts early because anomalies surface in the initial routing stage rather than after settlement. Merchants benefit when systems share real-time risk scores between POS devices and backend processors, allowing terminals to prompt for additional verification on flagged items.

By May 2026, updates to industry standards have expanded the use of tokenization within these trails, replacing actual card numbers with unique identifiers that still permit full tracing during investigations. Token service providers maintain mapping tables that authorized parties can query, preserving the integrity of the authorization history without increasing exposure. The European Central Bank has published guidance on these token frameworks, emphasizing their role in reducing data breach impacts across cross-border retail operations. Meanwhile, reports from the Australian Payments Network highlight how similar token practices have lowered fraud rates in subscription-linked POS environments.

Incorporating Automated Renewals Into Existing Authorization Flows

Automated renewals connect to the broader network by referencing stored authorization details rather than creating entirely new trails each cycle. Systems validate that the renewal amount, frequency, and merchant identifier align with the original customer consent captured during the first transaction. When patterns shift, such as a change in billing address or device used, the coordinated platform initiates step-up authentication before processing continues. This method keeps the transaction history intact while adapting to legitimate customer updates.

Retailers often integrate these renewal mechanisms through application programming interfaces that pull real-time status from the central authorization ledger. The ledger logs every renewal attempt alongside the parent transaction record, enabling quick resolution of chargebacks or account updates. Observers point out that maintaining this linkage prevents orphaned records that could otherwise complicate compliance audits or customer service inquiries.

Security Standards and Regulatory Alignment

Industry frameworks require encryption at every stage of the transaction trail, and coordinated systems enforce these rules through mandatory certification programs for devices and software. Payment Card Industry Data Security Standards outline specific controls for protecting authorization messages in transit and at rest, while also addressing how recurring billing data should be segmented from standard POS traffic. Compliance audits verify that audit logs remain immutable and accessible for the required retention periods.

Geographic variations appear in how regulators approach recurring payments. Canadian authorities focus on consumer notification requirements before renewal processing, whereas frameworks in other regions emphasize technical controls around data minimization. Merchants operating across borders therefore configure their coordinated platforms to apply the strictest applicable rules to each transaction trail segment.

Conclusion

Coordinated systems succeed in managing credit card authorizations and fraud prevention because they preserve complete, queryable trails from initial POS interaction through automated renewal cycles. These pathways support rapid decision-making at each network node while enabling retrospective analysis when needed. As networks evolve, continued emphasis on standardized messaging, tokenization, and cross-referenced analytics sustains both operational efficiency and protective measures for merchants and cardholders alike.